Successful startups experience four stages of growth. The most fascinating stage that is the least attractive and most crucial is “The Blade Years”; the first three years when revenue and growth are low. Read More

Posts Tagged ‘hockey stick growth’

Thoughts for entrepreneurs from someone who's been in the trenches.

Why Can’t You Make It Work with Spaghetti?

In which convincing buyers of your value proposition is maddening…and what to do about it.

When researching The Hockey Stick Principles, I felt that the founder of software firm Sageworks, Brian Hamilton, was the most profound with his explanations for startup challenges. Especially thoughtful was his analogy for how difficult it is to convince customers of your new idea: Read More

1-Minute Rant: “Play Something I Can Win!”

Discovering sales and marketing success is about incessantly trying different techniques. Otherwise, how will you know which processes will work best? Read More

In Love With Lean Startup? There Are Other Fish in the Entrepreneurial Sea

The Lean Startup methods are hot; I’m talking, “You can’t touch this” hot, a la M.C. Hammer. At least that’s how it felt to me while attending last month’s Lean Startup Conference where more than 1,500 gathered to pay homage to Lean methods (Lean). It’s spreading like wildfire across the globe with workshops and follow-up books.

Lean methods are not off-base. I know a few entrepreneurs who have successfully launched using Lean. If you aren’t familiar with Lean methods, they were originally attributed to Toyota for its manufacturing process to eliminate waste and build only what the customer wants. Professor and entrepreneur Steve Blank smartly applied Toyota’s ideas to start-ups. Then, Blank’s student, Eric Ries built upon his ideas from his own experiences and wrote the bestselling book The Lean Startup because the ideas worked so brilliantly. Much of the basis for Lean is rapidly validating or invalidating assumptions you made about your proposed business model by interviewing people and collecting data. Lean advocates for rapid prototyping and market testing.

Lean methods are not off-base. I know a few entrepreneurs who have successfully launched using Lean. If you aren’t familiar with Lean methods, they were originally attributed to Toyota for its manufacturing process to eliminate waste and build only what the customer wants. Professor and entrepreneur Steve Blank smartly applied Toyota’s ideas to start-ups. Then, Blank’s student, Eric Ries built upon his ideas from his own experiences and wrote the bestselling book The Lean Startup because the ideas worked so brilliantly. Much of the basis for Lean is rapidly validating or invalidating assumptions you made about your proposed business model by interviewing people and collecting data. Lean advocates for rapid prototyping and market testing.

But what rubs me wrong is the intimation that any process other than Lean is waaaaay off-base. For example, an attendee at the Lean Startup Conference who runs a university entrepreneurship center said to a group: “If university entrepreneurial centers aren’t deploying Lean methods, I’m to the point of calling it malpractice.” Malpractice? Really? For something as artful as starting an innovative company?

One speaker was explaining that if you don’t receive positive feedback during your first interviews, then you should pivot and try other business models. But when I told him that upon starting my own business, First Research I didn’t pivot (despite some less than stellar feedback) but instead stuck with my original plan until I landed paying customers, his response was that I was “perhaps lucky” and that I probably did pivot as I went along. (Partially true; I tweaked and improved my approaches.) He said Lean would have improved my chances of success. But would it have?

Please don’t misunderstand me. Lean is terrific, and if you’re starting a business, you should become aware of its methods and read Eric’s book. But there are Achilles’ heels you should also be aware of. Here are a few:

- Customers are not visionaries: Lean heavily relies upon asking potential customers what they really want, and then changing based upon their feedback. Yet Steve Jobs famously said, “We built [the Mac] for ourselves. We were the group of people who were going to judge whether it was great or not. We weren’t going to go out and do market research. We just wanted to build the best thing we could build.”[i] Jobs isn’t alone. Henry Ford once said, “If I had asked people what they wanted, they would have said faster horses.” The best-of-the-best entrepreneurs are visionaries and have good insight (or instinct) into what business models will work and which ones won’t. This is the “sixth sense” for business. So sometimes good ideas require your own intuition (not a future customer’s intuition) and most of all, the persistence to see them through to success.

- Giving up too soon may be a mistake: Lean relies upon “rapid” discovery and avoiding pouring good time and money after bad ideas. Yet the truth about when to give up on your idea or aspects of your business model may rest somewhere in between. Sometimes persistence is the trait that makes founders successful, and I can validate that from my own startup experiences. The key is knowing the difference between when your idea is a good one…despite poor feedback…versus when you should punt because the idea simply won’t work.

- “Early adopter” customers are hard to find: Lean heavily relies upon conversations to validate or invalidate your assumptions. But “early adopters” or “innovators”– those who are quick to try a new idea– are rare. Some studies show that only 2.5 percent of people fit into this category. So when you try interviewing the other 97.5 percent, how capable are they of validating your assumptions? Often times, you have to educate the market that it has a problem and that your product will fix it. This process requires lots of time and finding a few early adopters who are willing to be on the leading edge of change.

- There are no set formulas for starting a business: Many aspects of Lean rely upon data accumulation and scientific-type methods. Yet start-ups are more like art projects than science experiments; they are fluid, and each one is created subtly or profoundly different from another. Any founder must apply multiple experiences and thought processes to make it successful. Lean methods are good, but so are other strategies such as persistence or releasing a finished product.

- You’ll learn the most from your early selling efforts: Lean advocates for lots of interviews and conversations before you invest much money into a prototype. This is a fine idea, but you can only learn so much from talking to people because, as I’ve discovered, each person will say something completely different from another. Maybe I’m old-school, but the best way to learn is through trying to sell your product or idea. When you ask for people’s money, that’s when you get true objections and honest feedback.

At the conference, an executive form GE articulated how Lean greatly improved the speed and efficiency by which that company introduces new products. I have no doubt. But what’s good for GE may or may not be good for you if you’re starting your own business. There are many ways to go about it. I’m not saying that Lean isn’t a good way to build a start-up… but it definitely isn’t the only way. And while Lean may be hot, it can be touched. Stop. Hammertime. Oh. Oh-oh. Oh. Oh.

[i] “Playboy Interview: Steve Jobs, by David Sheff, Playboy,” Longform.org, August 28, 2015, http://longform.org/stories/playboy-interview-steve-jobs

1-Minute Rant: “Quality vs. Quantity Quandary”

One of the main goals of being a founder is to get stuff done. But getting stuff done and getting it done right means quality often suffers. Learn about balancing quality versus quantity in this week’s one-minute rant. Read More

Why My Publisher Cut “What it Really Takes” From My Entrepreneurship Book

My publisher cut Chapter 2, “What it Really Takes,” from my upcoming book The Hockey Stick Principles and offered the following candid advice: “This is about entrepreneurship in general and doesn’t interest me as much.”

My publisher cut Chapter 2, “What it Really Takes,” from my upcoming book The Hockey Stick Principles and offered the following candid advice: “This is about entrepreneurship in general and doesn’t interest me as much.”

A central theme of the chapter was five “commonalities” I’d discovered about the successful entrepreneurs I’d interviewed while researching the book, such as:

- An undying curiosity and sense of joy in the knotty challenges of problem-solving

- A tough skin and resilience when encountering failure, which enables them to bounce back and persevere

- A flexibility of mind about their plans, both for themselves and for their company, which allows and even welcomes the inevitable changes the plan will require over time

- The combination of an inventor’s heart and skills with a good mind for management, or the good sense to recognize that they don’t have a business-management mind and must partner with someone who does

- An attitude of hope, which is not blind to the obstacles or delusional about setbacks, but which fortifies them with a persistently positive outlook about their ultimate success

Experts in entrepreneurship have devised many lists of the five, eight, 10 or more personality traits of successful entrepreneurs; you can find reams of them with a simple web search. One well-researched list is the subject of Stanford lecturer Amy Wilkinson’s book The Creator’s Code, which offers six attributes of extraordinary entrepreneurs…they:

- “…spot opportunities that others don’t see”

- “…focus on the future”

- “…continuously update their assumptions”

- “…hone the skill to turn setbacks into successes”

- “…bring together the brainpower of diverse individuals”

- “…unleash generosity by helping others”

Amy’s list and my list partially match up. I’ve seen other lists saying entrepreneurs are risk-takers, competitive, leaders, and believe in themselves. Bill Aulet, senior lecturer on entrepreneurship at MIT’s Sloan School of Management, when asked in a CNBC interview what the stereotypical entrepreneur is like, also highlighted how iconoclastic and headstrong entrepreneurs are: “First of all, they have the spirit of a pirate. ‘We’re doing things differently!’ They disrespect the existing authority. And this is what we at MIT call ‘creative irreverence’ or ‘taking on the man.’”[i] I would agree that some do this, but not all.

The point is: you can drive yourself crazy trying to see how well you line-up with all these lists; it’s like reading the symptoms for an illness on WebMD. But the fact is that there is no one definitive list. Forget the lists!

I think all of the characterization of the traits of entrepreneurs misses the central truth. If there is one key thing about successful entrepreneurship I have observed and that arises clearly out of my research, it is that success comes down to the doing; it’s not primarily about fitting a personality profile in some silly checklist, it’s about taking action.

I’m just glad my publisher knows what it really takes to write a successful book!

[i] CNBC video interview online: “Entrepreneurship guru: ‘Need the spirit of a pirate’ Thu, 8 Aug ’13 | 6:35 AM ET

King Solomon’s Wise Advice for Startup Founders

One of my favorite books in the Bible is Ecclesiastes. Written by Solomon, the King of Israel, it discusses life’s true meaning. Despite being written 3,000 years ago, it applies amazingly well to startup founders today. King Solomon had it all. Read More

The Timeless Lessons of Ben Franklin’s Startup (Part 3)

This is the third in a three part series on how Ben Franklin’s startup story teaches us that the methods by which startups are conceived, grown, and evolved are timeless.

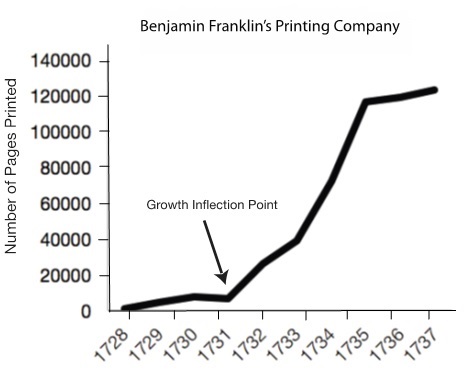

Hitting the Growth Inflection Point

Hitting the Growth Inflection Point

For five years, from 1724 to 1729, Ben had been a struggling founder who was attempting to find his way. He tried to open a business for two or three years without success, and then when he did open for business, he struggled with a lazy partner and debts. But Ben was a creative bootstrapper and learned methods to do work himself in order to save money, pay off loans, and eek by.

Much of Ben Franklin’s printing success in those early years was the result of his marketing creativity. He created popular writings that were remarkable and memorable—which he’d print and sell for a profit. He wrote like a modern-day blogger—providing entertaining, useful content in several subject areas. In 1733, under the pseudonym Richard Saunders, Franklin offered witty, worldly wisdom such as, “He’s a fool that makes his doctor his heir,” through his widely-read pamphlet Poor Richard’s Almanac.[i] To stand out, Franklin was the first to print cartoons and maps with his essays, the visuals increasing the appeal of his words.[ii]

Poor Richard helped Franklin’s printing business as its circulation grew to more than 10,000—keeping his presses busy. His creative content also helped him improve revenue at the Pennsylvania Gazette, the newspaper he had purchased, where advertising grew 42.5 percent under Ben’s management.[iii] This success also helped Franklin obtain larger print jobs, including being public printer for New Jersey and Delaware.

Five years after opening, Franklin’s forward-thinking print shop was now gaining momentum and was close to hitting a growth inflection point: “My business was now continually augmenting, and my circumstances growing daily easier, my newspaper having become very profitable…. I experienced, too, the truth of the observation, ‘that after getting the first hundred pound, it is more easy to get the second,’ money itself being of a prolific nature.”[iv]

Image courtesy of Archiving Early America

Surging Growth

Like many innovative businesses today, Franklin’s growth was also a result of his ability to duplicate good ideas. In 1733, Franklin entered into his first successful partnership with aspiring printers in other geographic locations. “The partnership at [South] Carolina having succeeded, I was encourag’d to engage in others, and to promote several of my workmen, who had behaved well, by establishing them with printing-houses in different colonies, on the same terms with that in Carolina. Most of them did well, being enabled at the end of our term, six years, to purchase the types of me and go on working for themselves, by which means several families were raised.”[v]

By 1748, when Franklin was 42 years old, his startup had grown into an empire of printing presses and publishing houses. Ready to take on new challenges, Franklin sold his printing company to his foreman, David Hall, in exchange for half the company’s profits for 18 years. Franklin’s payoff amounted to about 650 pounds annually ($943,044 in today’s dollars[vi]), after which he went on to discover processes, invent useful products, and play an important political role in effecting America’s independence from England by 1783 when the Treaty of Paris was signed.

The growth process of Benjamin Franklin’s printing startup resembles that of today’s innovative business startups. His success wasn’t predicated on detailed planning that, once followed, resulted in a quick success.

We unfortunately don’t have records of Franklin’s Printing Company’s annual revenue. As an alternative, I charted the estimated number of pages his company printed each year.[vii]

Every business you or I start today, therefore, is likely to follow the same growth curve as Ben’s printing business, one that calls for the same unflagging hard work, self-disciplined resilience to recover from periodic setbacks, and the fun of applying creative problem-solving in different ways again and again.

[i] (Franklin) 1733)

[ii] (Independence Nat’l Historical Park 2012)

[iii] (Miller 1974)

[iv] (Franklin 1996) p.51

[v] (Franklin 1996) p.51

[vi] Currency Conversion

[vii] Franklin’s Printwork.

1-Minute Rant: Health Insurance Costs are Killing Startups

In 1999 when I started First Research, if I had to purchase family health insurance at today’s prices, it would have cost me at least $2,000 per month – about as much as my entire monthly budget. I never could have afforded that; therefore, First Research would have never been started at all. Costs for purchasing health insurance are out of control, and it’s hitting startups hard. Hear me out! Read More

Twelve Reasons Selling Your Company Is a Bad Idea

It’s been nearly 10 years since I sold First Research for $26 million to Dun & Bradstreet. Do I regret doing so? It is a complex question, but let’s just go with YES. Here is why I encourage founders to think twice before selling their company:

- When you’re selling your business, you’re selling your passion: The words of one founder who made a great sale for his start-up especially resonate for me. Roger Bryan, who started Enfusen Digital Marketing, eloquently told mashable.com in an interview about his thoughts on the transaction, “I spent six years building the first company I sold. The day that I sold it was one of the greatest accomplishments of my life. . . .Then as each month went by, and the money sat in my bank account as I tried to figure out what to do next, the regret started to set in. I hadn’t sold my company; I had sold my passion.” Many founders feel a deep sense of remorse once a sale is complete, even if they have made a truly great deal.

- Most of the time, your “company” will becomes a “product”: Large businesses don’t normally maintain multiple independent departments for each product they sell. They already have a sales force, finance, and management – so why would they need those functions for your product? Cutting those duplicate expenses is one way mergers are profitable. The result is the destruction of the company you built.

- Merger negotiations are stressful: Selling your company is a full-time job – and keep in mind that you already have a full-time job managing your company that must maintain its current growth rate, which is probably fast. Life’s too short – trust me.

- Integration is stressful: Combining two organizations is like merging together two families. It’s a hellish two-year during which the acquiring firm must guess about which new business processes will work and which ones won’t. The stress is guaranteed to put gray hair on your head.

- Your employees often lose out: The first year after a merger, your employees are uncertain whether or not they’ll be fired—stressing everyone out. They’re told by the acquiring firm how “valuable” they are. But one important caveat—they aren’t told that they are only “valuable” for the first year or two after the merger. Screw that torture!

- The strategic fit between two companies can’t be known until they’re put together: The truth is that the acquiring company is only guessing about how successful integration will go – and they may have delusions of grandeur. Don’t assume that because a company is large and employs a bunch of MBAs and CPAs that they can foresee the future. Mergers are risky.

- You’ll be going through a not-so-great life-change: When I sold my company, I ended up with so much stress from integration and from losing something that I loved that I was visiting a psychologist and doctors to check my overall health. These stories don’t happen every time someone sells his or her company, but my research shows it happens quite often.

- You’ll probably want to rebuild what you already had: After selling their company, many founders, like myself, start a similar one all over again. To do that, you’ll have to grind out building a new business from scratch a second time.

- Having lots of money is overrated; owning a growing company is underrated: Just this morning, I was barking at the employees of my “yard irrigation company” because the system isn’t working properly and my expensive plants are dying. To my mind, that’s no way to live. Having lots of money is sort of cool, but having a high-energy growth company with a good culture is really, really cool!

- If you have a successful company, then you should have already earned money: Too many founders operate their company’s “breakeven” by investing all their operating profit into growth to increase their company’s valuation. Unless you are the next Amazon, why not pay out a reasonable percentage of profit as a dividend?

- It’s doubtful you’ll become “corporate jet rich” anyway: Corporate jet rich means you can afford several hundred thousand a year just for your jet. Ninety-nine percent of founders who sell their companies aren’t going to obtain that kind of wealth, so just keep your company and be happy with what you already have.

- Founders grow companies better than outsiders: A 2006 study showed that the average return on stocks of the 26 Fortune 500 firms run by founders was 18.5 percent annually from 1995 to 2005, which was seven percentage points better than the Fortune 500 average in those years. A 2010 study reported that “founding CEOs consistently beat the professional CEOs on a broad range of metrics ranging from capital efficiency (amount of funding raised), time to exit, exit valuations, and return on investment.”

The value of the satisfaction of guiding the long-term success of your company cannot be measured. When you sell out, you’re trying to quantify your creation, which doesn’t logically work. Ben Horowitz agrees in The Hard Thing About Hard Things, noting how the logical part is easy: “One of the most difficult decisions that a CEO ever makes is whether to sell her company. Logically, determining whether selling a company will be better in the long term than continuing to run it stand-alone involves a huge number of factors, most of which are speculative or unknown. And if you are the founder, the logical part is the easy part.”

To gain more valuable insight and perspectives about selling your business, check out John Warrillow’s podcast series Built to Sell Radio, a collection of well-organized interviews from founders who have sold their company. The best book on the subject is Finish Big by business writer Bo Burlingham.

By the way, I never could come up with 12 reasons you should sell your business. I’m just sayin’.

1-Minute Rant: My Solution to Reduce Health Care Costs

Health care costs are out of control. Here is one of the solutions on how I’d go about fixing this problem that is crippling startups. Read More

1-Minute Rant: “I’m in Charge! NO, I’m in Charge!”

This week’s VLOG

My decisions when managing my first start-up, First Research, weren’t perfect ones, but at least I made them quickly. Speed was my mantra! But if you want to do things slowly, log-jam your governance with fifty-fifty partnerships. Check out my rant.

1-Minute Rant: Three Tax Tips for Startup Founders

In this rant, I tell a story about how a friend of mine had to pay the IRS thousands of dollars unnecessarily that nearly broke him. Here are my three tips on how to avoid these tax pitfalls when starting your own startup. Read More

1-Minute Rant: “Impatience is a Virtue”

If you start a company with a new product, it’s important that you keep up a fast pace of development and get feedback from potential customers, suppliers, and retailers early. To do that, you’ve got to stress the speed of activity. Check out my video about how Julie Pickens, cofounder of Boogie Wipes, did just that:

1-Minute Rant: Product or Marketing? Which Wins Out?

This week’s rant addresses whether having a great product or having great marketing is more important for obtaining fast growth. I have my opinion. Find out my thoughts below! Read More

1-Minute Rant: “It’s What You Learn That Really Matters”

An aspiring entrepreneur recently told me about his idea, which involves creating online contests for personal home videos. (Nothing inappropriate—just good, clean fun.) He was walking me through the complexities involved with getting it going, telling me, “To even start this business, I’ll need at least $50,000. It’ll require secure hosting. Advertising is critical to getting enough customers to break even. I’ll need a business plan. I figure I’ll need X content entrants to break even at Y revenue per entrant.” He’d clearly put a good deal of thought into the concept, and he was already thinking seriously about its scalability.

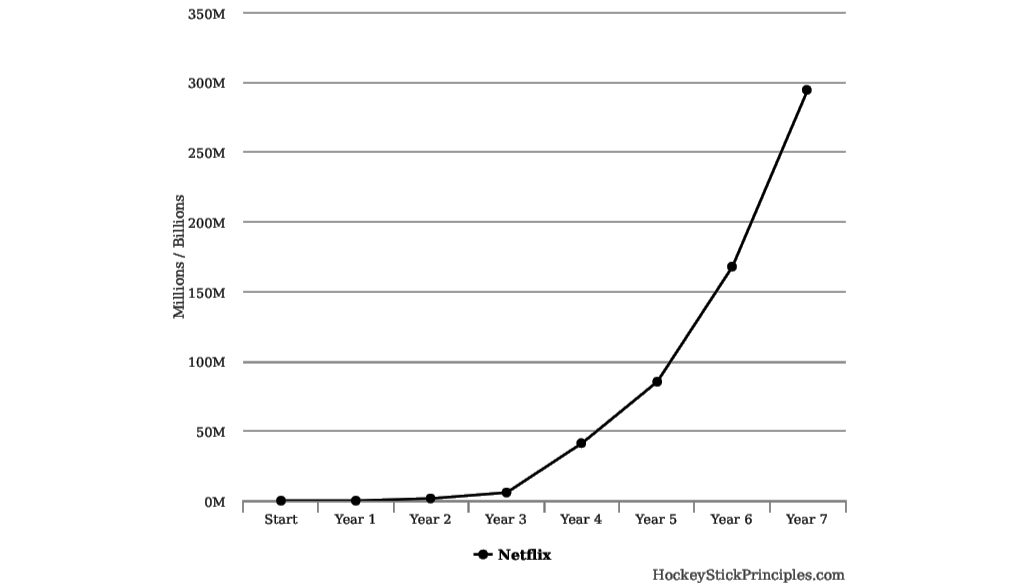

How Netflix Obtained Hockey Stick Growth (The Early Years)

Today, Netflix is wildly popular, and it seems just about everyone I know has a subscription. In 2017, it had more than $11.6 billion in revenue, but Netflix, just like many successful startups, started out as an idea hatched from its founder’s frustration. Read More

1-Minute Rant: “Screw Ups Happen”

One year ago, I published “Fifty Ways to Leave Your Lover” & Other Embarrassing Startup Moments”. I’ve done a lot of stupid things Read More

1-Minute Rant: “Why I Cut-Off My Email”

Let’s face it. Work-life balance is hard. Learn in this week’s Rant how not to get so consumed in the daily grind that you let life pass you by. Be creative, find your balance. I promise you’ll be way happier. Read More

1-Minute Rant: “Gettin’ Dirty”

Think about what we know about how Steve Jobs managed Apple. Read More

6 Questions You Should Ask Before Quitting Your Startup

On March 14, 1994, Sports Illustrated published, “Bag It, Michael” about how the basketball star Michael Jordan should give up playing baseball after only 11 months. I wonder what questions Jordan asked himself before quitting baseball? Did he give up too soon? If he’d stuck with it, could he have become an All-Star? We’ll never know. Read More

The One Thing that Prevents Most Startups from Succeeding

Why do so many startups struggle getting off the ground?

First, let’s begin with their products. Most new products are incomplete (explained in Geoffrey Moore’s excellent book, Crossing the Chasm); they lack features that users expect; they have no brand name recognition; their teams are “two guys and a dog”; the problem the product is solving is yet to be obvious to most buyers; they don’t have competitors to validate their value. Read More

1-Minute Rant: When “I Don’t Know” is Just Right

Why, as founders, do we feel the need to put a stake in the ground for what type of company we want to build? Maybe we should consider another approach. I explain why in this week’s 1-Minute Rant. Read More

1-Minute Rant: “Pitch Perfect”

One of my favorite arcade games growing up was Galaga. I dominated, but the coolest part was at the end it told me the percentage of shots hit versus missed. Read More

Let’s Not Allow Startups to Continue to Fall by the Wayside

A few weeks ago, the Brookings Institute released a fascinating study that shows startups are slowly disappearing. Read and weep: Read More

How to Negotiate Over-the-top Sales Contracts with Big Companies

“This is a fairly typical ‘big [company] MSA [Master Services Agreement], with lots of overreach and terms that are not applicable to the nature of your services. This is why the issues list is lengthy.”

-Email from my attorney after reviewing a sales agreement with a large company

6 Reasons Startups are Disappearing

Last week, I discussed that startups are slowly disappearing. The overwhelming question I received from readers was: Why are startups disappearing? Read More

The “How?” is the Hardest Part

Musician Tom Petty reminds us that “the waiting is the hardest part.” Here is how he went about writing this song that became such a classic with a sharp lesson.

But in entrepreneurship, the waiting isn’t the hardest part; it’s the “how?” that’s the hardest. Read More

1-Minute Rant: How Dare Those Salespeople!

Think carefully about how your salespeople are incentivized. Instead of blaming them for your startup’s problems, we as founders should take a step back – and consider why and where the real problems exist. Read More

1-Minute Rant: “Get a Life, Get a Hobby”

I would consider myself a pretty passionate person, especially when it comes to things I enjoy. I am passionate about my startups, my family, hiking, fishing and especially tennis. Read More

The Five Essential Commonalities for the Entrepreneurial Spirit

What does it take to be successful starting an innovative company? While writing The Hockey Stick Principles, I identified five fundamental elements of what I’ll call the “entrepreneurial spirit” that seem to be those that are most important in allowing founders to make it through the confusing, chaotic building process: Read More